Co-op's Dean Harris Explains How Convenience Media Built Its Own Category

In early 2023, retail media was forecast to grow at 15 percent year on year. Co-op’s own internal projections came in at less than half that figure. Dean Harris, Retail Media Leader at Co-op, told Retail Media Pioneers exactly why. The business had no clear market position. It had no compelling value proposition for advertisers. It had no focused strategy guiding its media and data investments. For more than a decade before that point, Co-op had been judged against supermarket media networks on metrics like basket size, a comparison that inevitably made a convenience retailer look weaker.

The fix Harris described was not a tweak. It was a full repositioning. Co-op chose to define itself as a convenience media network rather than compete inside the supermarket category, a move he acknowledged carried real risk. “Difference can be boutique, can be niche, can be nice to have,” he said. He described the danger of being seen as a smaller, optional add-on to the grocery media conversation rather than a distinct channel in its own right.

To avoid that outcome, Co-op invested in global thought leadership studies designed to prove the value of convenience as a category. It then shared that research openly with convenience retailers in Scandinavia, the US, Mexico, and Australia. “If we make the whole industry value convenience media, it also supports Co-op in the UK market,” Harris said.

Harris rejected the idea that shopping habits split neatly into online and offline. Convenience is unplanned and impromptu. It’s built around single-item missions rather than a weekly list, and it plays out across vans, mopeds, trolleys, and quick-commerce apps as much as physical stores.

Co-op stores sit in every UK postcode area. Seventy percent of the population lives within two miles of one of its 2,350 locations, including branches inside music venues, university campuses, hospitals, and military bases. Ninety percent of convenience sales happen in-store, compared with 80 to 85 percent for grocery overall. That gives Co-op a targeting opportunity, by category, mission, demographics, and location, that a pure eCommerce comparison would miss entirely.

The frequency numbers back up the positioning. Co-op holds roughly 5.5 percent market share and ranks seventh in UK grocery by size. Yet its shoppers visit 125 times a year, 25 percent higher than the next retailer on the list. Harris described those visits as individual moments rather than generic footfall. Each one is an opportunity for a brand to be chosen for a specific mission, whether that’s a top-up shop, a treat, or a weekend indulgence.

One recurring doubt about convenience media is that low dwell time in small stores limits its ability to build long-term brand metrics like mental availability. Harris said Co-op tested that assumption directly. It partnered with Lumen Research, whose eye-tracking and attention data feeds major media planning tools globally.

The results ran against the assumption. Convenience stores lack the aisle signage of a large supermarket, so shoppers rely more heavily on advertising to navigate the store. That produces roughly double the visibility per visit and more than double the viewing time. Combined, Harris said, this works out to quadruple the attentive seconds per thousand people compared with a standard grocery environment. “Attention is a consumer-centric metric,” he said, contrasting it with impressions, which he called a publisher-centric one.

Harris shared a beer brand campaign run with Circana, which holds store and line-item sales data across every UK retailer. Circana compared Co-op stores where the campaign ran against stores where it didn’t, then looked at rival stores in the same catchment areas.

Co-op’s own stores showed a 12 percent brand sales increase. But nearby competitor stores with no direct ad exposure still saw a statistically significant 3 percent increase. Harris attributed this to shoppers who saw the ad in Co-op and later bought the product elsewhere. Once he factored in that halo effect, the campaign had generated nearly five times the incremental sales that Co-op’s own closed-loop measurement alone would have shown.

“We were one of the first in the world to report on market-wide incremental sales from an in-store retail media campaign.”

That evidence shaped Co-op’s next product decisions directly. Since October, the retailer has installed digital screens in store entrances at a rate of 25 a week. It now has 850 screens nationally and aims to pass 1,000, all targetable by category, mission, and location, with time-of-day and weather targeting planned next.

Harris also described reframing Co-op’s loyalty proposition around “addressable moments” rather than raw membership scale. Co-op’s loyalty base runs at roughly a third the size of programs from Tesco, Sainsbury’s, or Boots. Rather than compete on scale, Co-op built a simpler three-step booking process for off-site media: pick a mission, choose a category, select a channel.

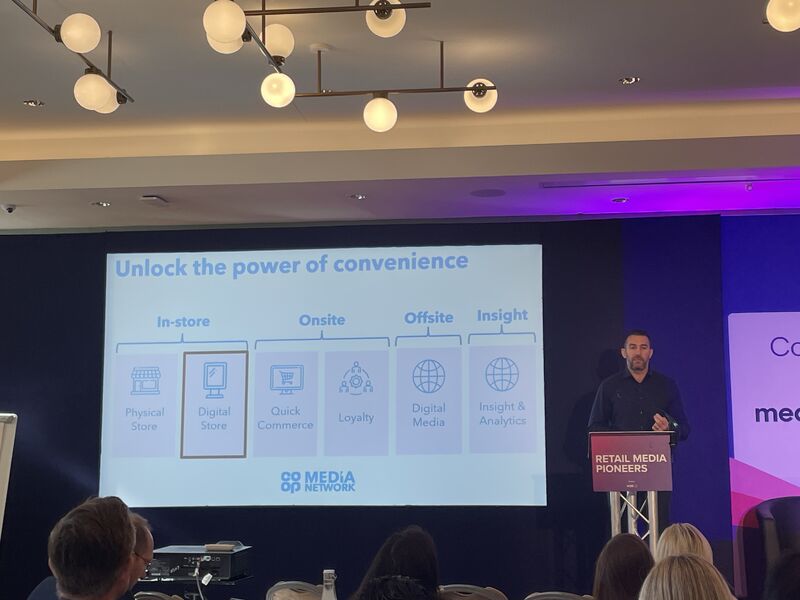

Harris closed with three takeaways for the room. Think in terms of moments, not just sales or people. Plan media in a consumer-centric way that measures attention rather than impressions. Treat retail media as one combined strategy rather than six isolated channels run in parallel.

“Convenience is different,” he said, “and it demonstrates the value, but it’s complementary.”

Leave a Reply

You must be logged in to post a comment.